Alphabet: Between Advertising Dominance and the AI Bet, a Tech Giant's Strategic Transformation

- Administrateur

- Apr 23

- 3 min read

A technology conglomerate built around three pillars

Alphabet, Google's parent company since its 2015 reorganization, remains one of the most influential players in the global digital economy. The group structures its business around three main segments: Google Services (Search, YouTube, Android, Chrome, Play Store, subscriptions), Google Cloud (infrastructure, platform, and Workspace solutions), and Other Bets (technology ventures such as Waymo, Verily, and Isomorphic Labs). Corporate-level activities, including AI investments held directly at the holding level, complete the picture.

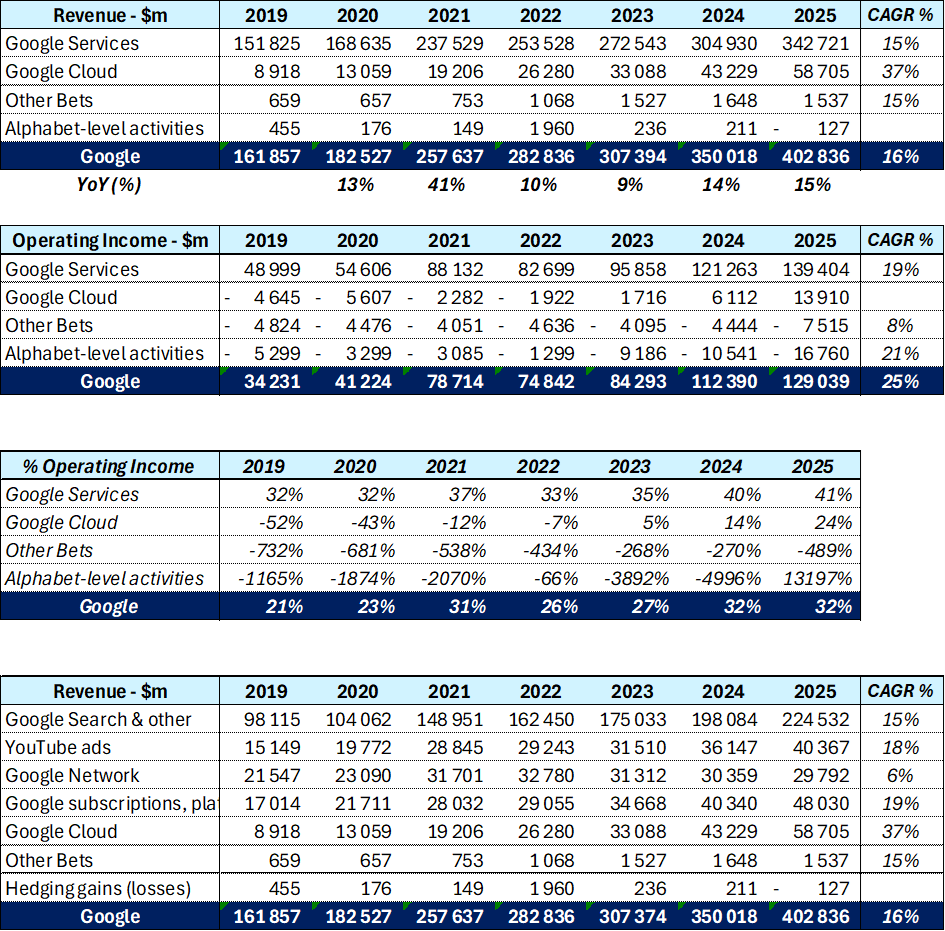

In 2025, Alphabet posted revenue of 402.8B (32% margin). Over 2019-2025, the group delivered a 16% revenue CAGR and a 25% operating income CAGR, reflecting powerful operating leverage, particularly driven by the Cloud turnaround.

Strategic levers refocused on AI and Cloud

Google Services remains the core engine, generating 342.7Bin2025(85 224.5B, +13% YoY) maintains its dominant position despite competitive pressure from conversational engines (ChatGPT, Perplexity). YouTube Ads ($40.4B, 18% CAGR) consolidates its position as the global video leader, while subscriptions (YouTube Premium, YouTube TV, Google One) reach $48B (19% CAGR), reflecting a successful pivot toward recurring revenue.

Google Cloud is now the most strategic growth driver: $ 58.7B revenue in 2025 (+36%), with operating margin surging to 24%, compared with -52% in 2019. The franchise has been structurally profitable since 2023, capturing demand tied to generative AI (Vertex AI, Gemini, TPUs). A record cloud backlog confirms Google's credible positioning against AWS and Azure.

Other Bets remain marginal ( $ 1.5B revenue) and loss-making (-$7.5B), but embody long-term optionality, notably via Waymo, whose robotaxi deployment is accelerating in the U.S.

Intensifying competition on all fronts

Alphabet operates in an unprecedented competitive environment. In Search, the rise of LLMs challenges the historical sponsored-links model. In Cloud, AWS and Microsoft Azure retain the market share lead. In AI, Microsoft-OpenAI, Meta, Anthropic, and Chinese players (DeepSeek, Alibaba) are driving an unprecedented capex race. Lastly, regulatory pressure (DOJ antitrust on Search and Ad Tech, European DMA) remains a major risk factor, with the potential for partial divestiture of Chrome or advertising activities.

Recent news: AI acceleration and financial discipline

The latest results confirm the thesis of successful AI monetization. The integration of Gemini into Search via "AI Overviews" has not cannibalized ad revenue as the market feared. On the contrary, Google Services shows spectacular margin expansion (+6 points in two years), supported by operating leverage and cost-reduction plans launched in late 2023.

Cloud operating margins have multiplied, validating the massive infrastructure investment strategy. 2025 capex should exceed $75B, mainly dedicated to data centers and in-house TPUs—a differentiator against Nvidia-dependent hyperscalers.

On the capital allocation front, Alphabet maintains a generous shareholder policy: buyback program exceeding $ 70B and sustained dividend initiated in 2024. Free cash flow generation remains massive, providing rare strategic flexibility.

Points of vigilance and outlook

Three risks deserve investor attention. First, capex sustainability: the capital intensity of Cloud and AI could weigh on free cash flow if monetization lags. Second, regulatory risk: an adverse ruling on Chrome or Ad Tech could significantly impair valuation. Third, the disruption of Search remains the most structurally concerning scenario, even though current figures contradict the most pessimistic theses.

Conversely, positive catalysts are numerous: Gemini's rise, Waymo's commercial deployment, Cloud acceleration, and continued cost optimization. With a consolidated operating margin of 32% and double-digit growth, Alphabet offers a rare profile of combined value and growth, provided one believes in its ability to defend its advertising rent throughout the AI transition.

Comments