PDD Holdings: Between Chinese Dominance and Global Offensive, the Temu Model Tested by Headwinds

- Administrateur

- Apr 29

- 2 min read

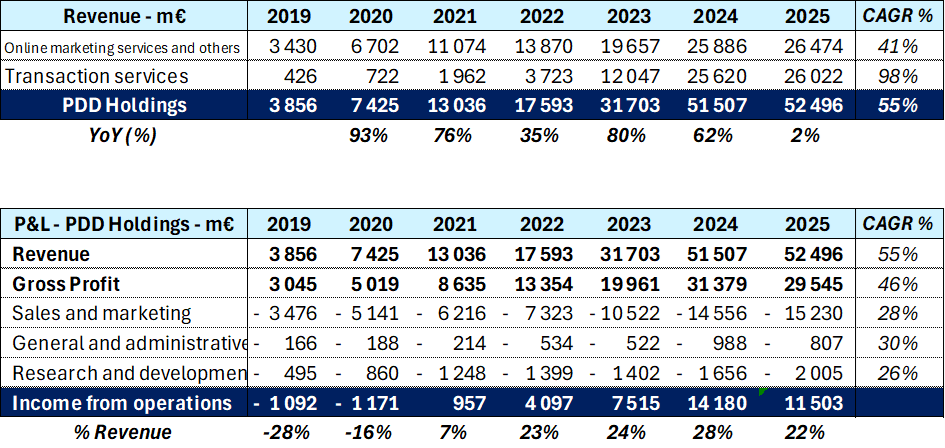

PDD Holdings, listed on Nasdaq under the ticker PDD, has emerged in less than a decade as one of the most disruptive players in global e-commerce. Founded in 2015 with the launch of Pinduoduo in China, the company led by Lei Chen now operates two flagship platforms: Pinduoduo, which dominates the social and agricultural e-commerce segment in China, and Temu, its international spearhead launched in September 2022, now present in more than 80 markets.

Strategic levers and competitive positioning

The PDD model rests on three pillars: direct sourcing from manufacturers (C2M model – Consumer-to-Manufacturer), a viral engagement mechanism through group buying and social discounts, and an increasingly internalized logistics infrastructure. In the Chinese market, Pinduoduo has prevailed over Alibaba and JD by capturing consumers in tier-three and tier-four cities, who are particularly price-sensitive. This expanded base represents a major defensive asset in a context of sluggish Chinese consumption.

Internationally, Temu directly targets Amazon, Shein, and AliExpress with a deep-discount strategy enabled by the direct-from-China shipping model under the de minimis threshold. This pricing aggressiveness has translated into colossal marketing expenditures – Temu was among the largest advertisers on Meta and Google in 2023-2024 – but also into pressured margins. Competition is intensifying with Shein, which is preparing its IPO, and with the accelerated expansion of TikTok Shop, particularly in the U.S. market.

Recent developments: regulatory pressure and strategic inflection

2024-2025 marked a turning point for PDD. The announced and effective elimination of the U.S. de minimis exemption (the USD 800 threshold allowing duty-free entry) for Chinese parcels constitutes a structural shock for Temu. This decision, signed by the Trump administration in February 2025 and then extended to all origins from May 2025, forces the platform to rethink its logistics model: accelerated development of the "semi-managed model" with local U.S. warehousing, partnerships with sellers already holding U.S. inventory, and geographic diversification toward Europe, Latin America, and the Middle East.

Specific points to monitor

Three issues frame the medium-term investment thesis. First, the resilience of the Temu model post-de minimis: the ability to maintain pricing advantage while absorbing tariffs and localizing inventories will determine the international growth trajectory. Second, the monetization of Pinduoduo in China, in a fragile macroeconomic environment and facing Alibaba's (Taobao) counterattack in the low-cost segment. Third, geopolitical and regulatory risk, with growing exposure to U.S.-China tensions, European product compliance investigations, and data protection concerns.

Governance is also a recurring concern: relative opacity of management, lack of detailed guidance, and the VIE structure typical of Chinese companies listed in the U.S. expose the stock to a persistent discount. However, the balance sheet remains strong, with net cash exceeding USD 50 billion, providing considerable leeway to navigate this transition phase.

PDD Holdings illustrates the tension between remarkable operational execution and an increasingly hostile geopolitical environment. For expert investors, the current valuation – significantly discounted compared to U.S. peers – may constitute an asymmetric opportunity, provided one accepts high volatility and limited visibility. The coming year will be decisive in validating the group's ability to transform Temu into a sustainable global platform rather than a cyclical phenomenon.

Comments